Is Value Investing Dead, Again?

Given the dramatic underperformance of value stocks (vs. growth stocks) in recent years, it’s understandable that people would question the validity of the strategy, perhaps believing that the value “premium” has vanished. But observers of market history know that value faced similar death sentences previously, only to stage a dramatic comeback and deliver spectacular returns.

I used the word “again” in the title because this is not the first nor the last time that value investing will be declared, DEAD. History always repeats itself – maybe not exactly, but in variations. In the investing world this is no different.

When people ask me, “what is value investing?” I say it’s trying to buy a dollar for 75 cents. Which is an oversimplification but it makes perfect sense to regular people. So what is growth investing? It’s buying 75 cents for a dollar with the expectation that 75 cents becomes $5.00 in time. Both strategies are completely valid, and thus we invest in both types of companies. All of our investment portfolios have exposure to both value stocks and growth stocks.

Growth stocks are companies you talk about at the water cooler – think Apple, Amazon, Facebook, Netflix, etc. They tend to be in tech industries (telecommunications, electronics, software, etc.) Their products are fun and exciting and we use them daily. Value companies develop products we use on a regular basis too, but they tend to be boring and predictable. When was the last time you heard someone say, “hey, have you heard about the latest laundry detergent that Procter & Gamble is developing?”

It just so happens that in the current environment value stocks are getting their ass kicked by growth stocks, and have been for some time. It’s no secret that we “tilt” our portfolios in favor of the cheaper (value) portion of the stock market. Why do we do this? Because 100 years of historical stock prices have provided convincing evidence that value stocks tend to outperform over long periods of time.

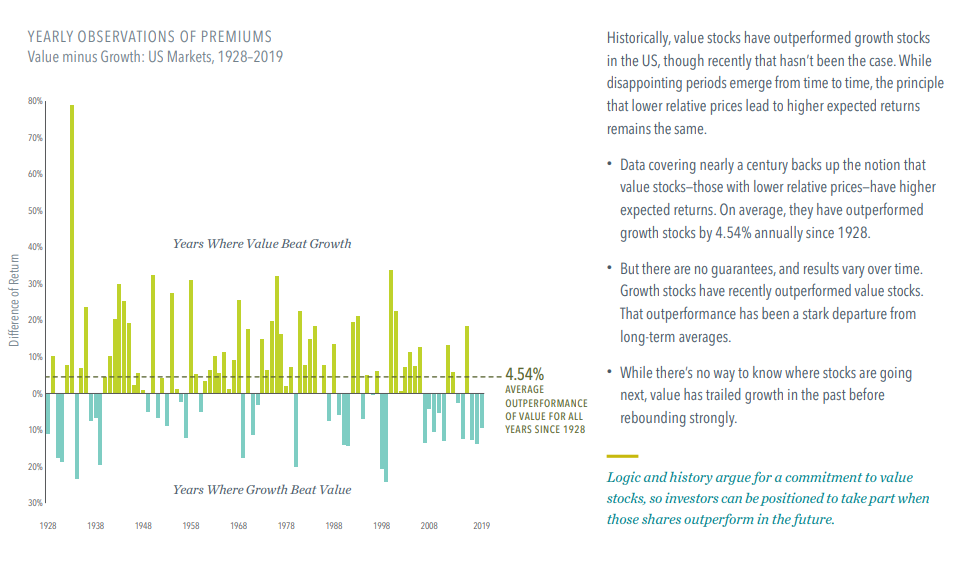

I can’t explain it any better than this visual representation of the value premium through the years. We are simply following the evidence and, so far, history has been on value’s side vs. growth. Of course this data has been compiled over a very long period of time, and there are going to be shorter time frames where this value premium is negative. Clearly we are in one of those periods now.

So this may lead to a seemingly logical question – if we are in a period where value is underperforming dramatically, why not get out in favor of growth until the trend reverses? We cannot time when this trend will reverse, just as we cannot time the ups and downs of the stock market in general. And these reversals usually happen with no warning and at breakneck speed.

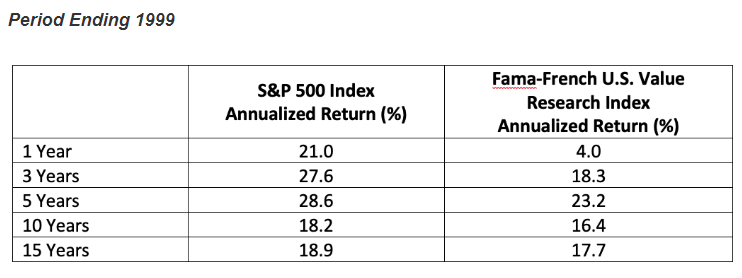

Let’s look at an example in recent history. Traveling back to 1998-1999, when the value “premium” was a cumulative -32%, value had been declared dead. And value investors like Warren Buffett looked like fools.

By the end of 1999, value had underperformed in 1,3,5,10, and 15 year rolling periods. Ouch. I might point out that the returns value produced were still fantastic – they just didn’t look so hot compared to the S&P 500 or growth stocks.

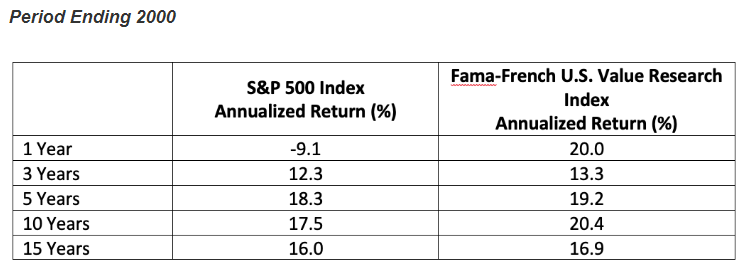

Fast forward just one single year, and value stocks outperformed over each of the periods. The lessons are that there is a lot of volatility in the value premium, and that even long periods of underperformance can be reversed over very short time frames.

Over the next 17 years (2000-2016), the Russell 3000 Value Index outperformed the Russell 3000 Index by 147 percentage points in terms of total return (207.5% vs. 60.3%).

Underperformance of Value Funds in Your Portfolio

I also want to address the issue of “underperformance” of the value funds in your portfolio. Many of you hold Dimensional Funds (DFA) in your portfolios, as these are our preferred vehicles for capturing the value premium. When value is out of favor, it’s easy to call out DFA as the cause of underperformance. I assure you it is not a mismanagement of funds or poor stock picking that has caused this. It’s simply a function of value being the most beaten-down portion of the market right now.

Just observe the year-to-date performance of the two most prominent benchmark indexes for value funds:

Russell 1000 Value (Large-Cap Value Stocks): -16%

Russell 2000 Value (Small-Cap Value Stocks): -26%

If you are a value stock manager you cannot hide from this if you are true to your investment strategy and convicted in your philosophy.

DFA is the most consistently “value” of all the value managers on the planet. So, when the value premium is working they look like rock stars. When it’s not, they look like dullards. It comes with the territory.

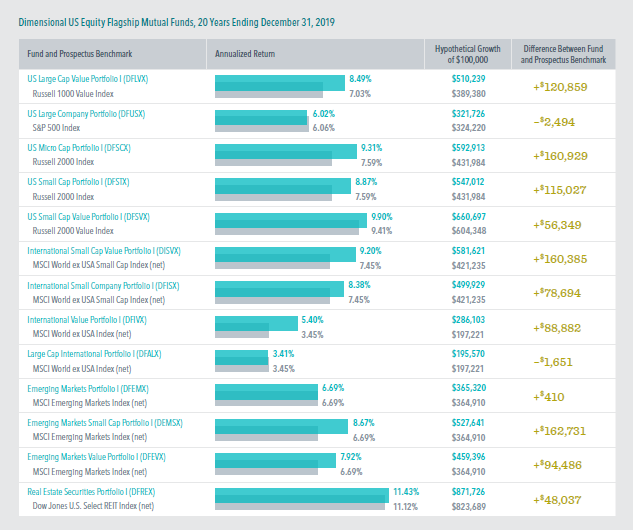

But if we look at their long-term track record of managing equity funds, you’ll see their results have been impressive. The vast majority of their equity funds have outperformed their benchmarks over a 20-year period. Most notably the US Large Cap Value (DFLVX) and US Small Cap Value (DFSVX) funds which many of you hold in your portfolios. For a full PDF version of this report click here.

When comparing DFA to other funds, I think you’ll find it difficult to find funds that have even been around longer than 10 years.

Where the Performance is Coming From

I think it’s important to understand where most of the performance of this 2020 market is coming from. Let’s compare two ETFs: SPY (SPDR S&P 500 ETF) and RSP (Invesco S&P Equal Weight ETF).

SPY represents the standard, market-cap weighted S&P 500 index. The one you see highlighted in the financial media every second of every day. SPY is market-cap weighted – meaning the pricier, larger stocks will dominate the index. RSP represents the same S&P 500 Index, only it weights the component companies in exactly equal weights. The two ETFs hold the exact same stocks, just in very different proportions.

Their year-to-date performance numbers are like the tale of two cities:

SPY (SPDR S&P 500 ETF): -0.72%

RSP (Invesco S&P Equal Weight ETF): -10.59%

SPY is basically flat while RSP has been left in the dust.

In the market cap-weighted version (SPY), the top five stocks – Facebook, Amazon, Google, Apple, Microsoft) now represent 23% of the capitalization of the index (the last time this happened was 1999) and thus account for 23% of the returns. In RSP (equal-weight) these stocks have a weight of 1% (they’re just 5 out of 500 stocks).

When these stocks do well in the market-cap weighted index, the index itself will tend to look good. There’s nothing negative about this. This is just pure, market weighted exposure. We hold an S&P 500 ETF, so we love it when these stocks do well.

But we also understand that there will come a time when these large, dominant tech stocks will not be doing so well. And we’ll be glad that we have exposure to other, less expensive portions of the market.

Conclusion

Everyone wants to be the market when the market is kicking the pants off everything else. We’re just as frustrated with value and small-cap as anyone else right now. I hold the exact same funds in my portfolio and I hate seeing red! Rest assured that we are constantly evaluating our investments, and if there is a need for structural change we won’t hesitate to make that call.

But if history is any guide, this is a classic struggle between growth and value. I don’t think it’s time to shovel the dirt on value’s grave just yet. It will have it’s day in the sun again.

Is Value Investing Dead, Again?

Is Value Investing Dead, Again?

Given the dramatic underperformance of value stocks (vs. growth stocks) in recent years, it’s understandable that people would question the validity of the strategy, perhaps believing that the value “premium” has vanished. But observers of market history know that value faced similar death sentences previously, only to stage a dramatic comeback and deliver spectacular returns.

I used the word “again” in the title because this is not the first nor the last time that value investing will be declared, DEAD. History always repeats itself – maybe not exactly, but in variations. In the investing world this is no different.

When people ask me, “what is value investing?” I say it’s trying to buy a dollar for 75 cents. Which is an oversimplification but it makes perfect sense to regular people. So what is growth investing? It’s buying 75 cents for a dollar with the expectation that 75 cents becomes $5.00 in time. Both strategies are completely valid, and thus we invest in both types of companies. All of our investment portfolios have exposure to both value stocks and growth stocks.

Growth stocks are companies you talk about at the water cooler – think Apple, Amazon, Facebook, Netflix, etc. They tend to be in tech industries (telecommunications, electronics, software, etc.) Their products are fun and exciting and we use them daily. Value companies develop products we use on a regular basis too, but they tend to be boring and predictable. When was the last time you heard someone say, “hey, have you heard about the latest laundry detergent that Procter & Gamble is developing?”

It just so happens that in the current environment value stocks are getting their ass kicked by growth stocks, and have been for some time. It’s no secret that we “tilt” our portfolios in favor of the cheaper (value) portion of the stock market. Why do we do this? Because 100 years of historical stock prices have provided convincing evidence that value stocks tend to outperform over long periods of time.

I can’t explain it any better than this visual representation of the value premium through the years. We are simply following the evidence and, so far, history has been on value’s side vs. growth. Of course this data has been compiled over a very long period of time, and there are going to be shorter time frames where this value premium is negative. Clearly we are in one of those periods now.

So this may lead to a seemingly logical question – if we are in a period where value is underperforming dramatically, why not get out in favor of growth until the trend reverses? We cannot time when this trend will reverse, just as we cannot time the ups and downs of the stock market in general. And these reversals usually happen with no warning and at breakneck speed.

Let’s look at an example in recent history. Traveling back to 1998-1999, when the value “premium” was a cumulative -32%, value had been declared dead. And value investors like Warren Buffett looked like fools.

By the end of 1999, value had underperformed in 1,3,5,10, and 15 year rolling periods. Ouch. I might point out that the returns value produced were still fantastic – they just didn’t look so hot compared to the S&P 500 or growth stocks.

Fast forward just one single year, and value stocks outperformed over each of the periods. The lessons are that there is a lot of volatility in the value premium, and that even long periods of underperformance can be reversed over very short time frames.

Over the next 17 years (2000-2016), the Russell 3000 Value Index outperformed the Russell 3000 Index by 147 percentage points in terms of total return (207.5% vs. 60.3%).

Underperformance of Value Funds in Your Portfolio

I also want to address the issue of “underperformance” of the value funds in your portfolio. Many of you hold Dimensional Funds (DFA) in your portfolios, as these are our preferred vehicles for capturing the value premium. When value is out of favor, it’s easy to call out DFA as the cause of underperformance. I assure you it is not a mismanagement of funds or poor stock picking that has caused this. It’s simply a function of value being the most beaten-down portion of the market right now.

Just observe the year-to-date performance of the two most prominent benchmark indexes for value funds:

Russell 1000 Value (Large-Cap Value Stocks): -16%

Russell 2000 Value (Small-Cap Value Stocks): -26%

If you are a value stock manager you cannot hide from this if you are true to your investment strategy and convicted in your philosophy.

DFA is the most consistently “value” of all the value managers on the planet. So, when the value premium is working they look like rock stars. When it’s not, they look like dullards. It comes with the territory.

But if we look at their long-term track record of managing equity funds, you’ll see their results have been impressive. The vast majority of their equity funds have outperformed their benchmarks over a 20-year period. Most notably the US Large Cap Value (DFLVX) and US Small Cap Value (DFSVX) funds which many of you hold in your portfolios. For a full PDF version of this report click here.

When comparing DFA to other funds, I think you’ll find it difficult to find funds that have even been around longer than 10 years.

Where the Performance is Coming From

I think it’s important to understand where most of the performance of this 2020 market is coming from. Let’s compare two ETFs: SPY (SPDR S&P 500 ETF) and RSP (Invesco S&P Equal Weight ETF).

SPY represents the standard, market-cap weighted S&P 500 index. The one you see highlighted in the financial media every second of every day. SPY is market-cap weighted – meaning the pricier, larger stocks will dominate the index. RSP represents the same S&P 500 Index, only it weights the component companies in exactly equal weights. The two ETFs hold the exact same stocks, just in very different proportions.

Their year-to-date performance numbers are like the tale of two cities:

SPY (SPDR S&P 500 ETF): -0.72%

RSP (Invesco S&P Equal Weight ETF): -10.59%

SPY is basically flat while RSP has been left in the dust.

In the market cap-weighted version (SPY), the top five stocks – Facebook, Amazon, Google, Apple, Microsoft) now represent 23% of the capitalization of the index (the last time this happened was 1999) and thus account for 23% of the returns. In RSP (equal-weight) these stocks have a weight of 1% (they’re just 5 out of 500 stocks).

When these stocks do well in the market-cap weighted index, the index itself will tend to look good. There’s nothing negative about this. This is just pure, market weighted exposure. We hold an S&P 500 ETF, so we love it when these stocks do well.

But we also understand that there will come a time when these large, dominant tech stocks will not be doing so well. And we’ll be glad that we have exposure to other, less expensive portions of the market.

Conclusion

Everyone wants to be the market when the market is kicking the pants off everything else. We’re just as frustrated with value and small-cap as anyone else right now. I hold the exact same funds in my portfolio and I hate seeing red! Rest assured that we are constantly evaluating our investments, and if there is a need for structural change we won’t hesitate to make that call.

But if history is any guide, this is a classic struggle between growth and value. I don’t think it’s time to shovel the dirt on value’s grave just yet. It will have it’s day in the sun again.

Recent Posts

Financial Synergies Completes 20-Year Internal Succession, Names Eight New Partners

Monthly Market Update: Rising Policy Uncertainty Leads to Increased Market Volatility

Lessons from Warren Buffett for Today’s Investors

Subscribe to Our Blog

Shareholder | Chief Investment Officer